17 July, 2026

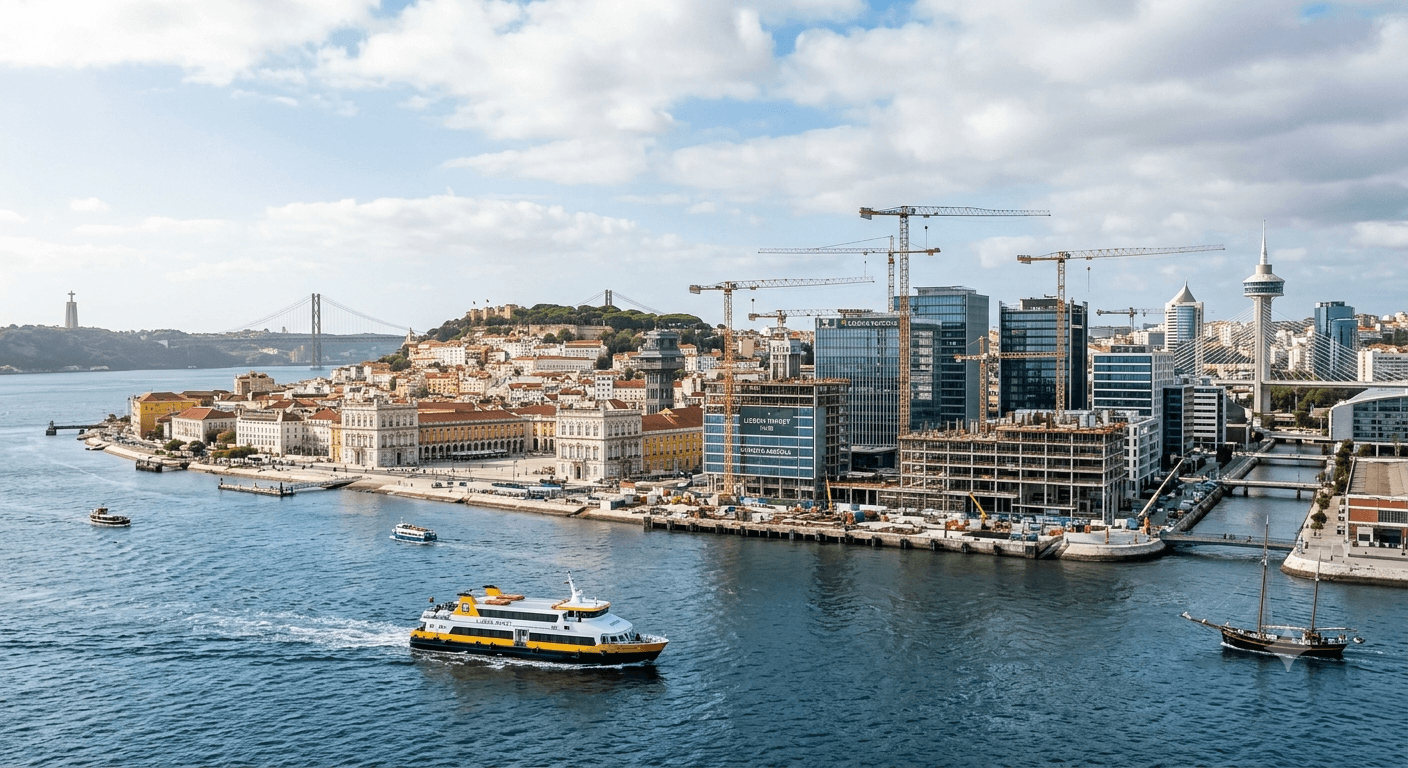

Portugal’s commercial real estate market opened 2026 on a strong footing. Despite a backdrop of global geopolitical uncertainty and softer domestic economic momentum, investment volumes climbed sharply year-on-year, prime rents pushed higher across several segments, and international capital continued to view the country as an attractive, income-generating market within the wider Iberian and European landscape.

Below, we break down what happened across investment, retail, hospitality, offices, industrial & logistics, during the first quarter of the year, drawing on multiple market research sources covering the Portuguese and broader European commercial property sectors.

Investment Volume: A Strong Start to the Year

Commercial real estate investment in Portugal reached figures ranging from roughly €892 million to €915 million in Q1 2026, representing year-on-year growth of somewhere between 34% and 41%. This marks one of the strongest opening quarters in recent years and sits well above the three-year Q1 average, with one estimate placing volumes as much as 130% above that benchmark.

The average deal size also increased, reaching approximately €32.5 million per transaction, roughly 2% higher than the prior year. Around 28 transactions were recorded in the quarter across the main data sets.

Key demand drivers included:

- Hospitality, which led sector allocation with roughly €340–360 million invested, equivalent to around 39% of total volume

- Retail, close behind with approximately €340 million, representing 37–38% of activity

- Industrial & Logistics, which posted the strongest year-on-year growth of any sector, albeit from a low base, supported by two data centre transactions

- Offices, which remained the weakest segment, capturing only 4–5% of volume and falling more than 50% year-on-year

Capital origin was notably international, with foreign investors accounting for roughly 56–78% of transaction volume depending on the source, led by capital from Spain, France, the United States and the United Kingdom. Domestic capital, however, showed renewed conviction, with Portuguese institutional players and asset managers accounting for a meaningful share of activity, particularly in retail.

Institutional investors and private equity together represented around 64% of all capital deployed, reinforcing Portugal’s reputation for attracting sophisticated, long-duration capital even amid global volatility.

Standout Deals of the Quarter

- Arrábida & Gaia Shopping (70% stake) – approximately €180 million, acquired by a new retail-focused investment vehicle from a Sierra-managed fund

- Penha Longa Resort – €120–140 million, a five-star hospitality asset sold to an international buyer consortium

- InterContinental Porto – €70–90 million, reportedly the highest price per key ever recorded for a standing hotel asset in Portugal, at roughly €714,000 per key

- Covilhã Data Centre – approximately €120 million, underscoring growing investor appetite for digital infrastructure

Retail: Shopping Centres and High Streets Stay in Demand

Retail remained one of the twin engines of the Portuguese investment market. Shopping centres captured the largest share of retail investment, supported by resilient footfall and sales growth, while retail parks continued to attract capital thanks to their convenience-led positioning and defensive income profile.

On the occupier side, Lisbon’s high street retail market recorded around 27 new store openings during the quarter, a 23% year-on-year increase, with the Baixa district drawing the highest number of openings. Prime rents on Rua Garrett and Rua Augusta reached €150/sqm/month, with evidence of deals closing above that threshold. Porto’s high street market also performed strongly, with 16 new openings and prime rents around €90/sqm/month on Rua de Santa Catarina.

Shopping centre performance stayed healthy too, with total sales up roughly 5% year-on-year and footfall rising around 7%. Prime shopping centre rents held at approximately €95–120/sqm/month in Lisbon and €75/sqm/month in Porto, while retail park rents remained close to €11–13/sqm/month nationally.

Vacancy in prime high street corridors continues to fall, nearing full occupancy in the most sought-after zones, and pushing retailers to consider secondary streets as the natural next step for expansion.

Hospitality: Record Pricing Continues

Hospitality was the standout performer of the quarter in several data sets, with investment volume up well over 100% year-on-year. International investors, favouring value-add strategies, drove much of this activity, with five-star assets accounting for the bulk of invested capital.

Hotel supply also expanded, with dozens of new hotels and several hundred new rooms added to the national stock during the quarter, concentrated mainly in Lisbon. Looking ahead, the pipeline for 2026 points to thousands of additional rooms, with further growth expected in 2027 and 2028.

Demand fundamentals remain solid: Portugal recorded around 82 million overnight stays and 33 million guests over the twelve months to March, both up year-on-year, with the United Kingdom and Germany the leading source markets and the United States the fastest-growing.

Offices: Selective and Supply-Constrained

The office sector told a more cautious story. Investment volume fell sharply year-on-year in most data sets, driven less by weak demand and more by a persistent pricing mismatch between buyers and sellers. Prime yields held stable at around 5.0%, and investor appetite remains highly selective, focused on prime locations and assets with strong occupational fundamentals.

Occupier demand, however, told a different story. Lisbon office take-up rose sharply year-on-year, supported by relocations to newly completed developments, while prime rents continued to climb, reaching around €32/sqm/month in the capital. Porto also saw a rebound in leasing activity, with international occupiers driving a majority of take-up. Vacancy rates remained broadly stable in both cities.

Rising rental levels are also encouraging some occupiers to consider purchasing rather than leasing their office space, a trend expected to continue through the year.

Industrial & Logistics: Undersupplied, Not Underperforming

Industrial and logistics investment surged year-on-year, largely on the back of a landmark data centre transaction, though overall leasing take-up softened compared to the same period last year. The sector continues to be shaped by a limited pipeline of prime assets rather than any lack of occupier or investor interest, with prime yields holding steady in the mid-5% to 6% range for big-box logistics in Lisbon and Porto.

Rental growth remained a consistent theme, with prime logistics rents in Greater Lisbon and Porto both edging higher, and further increases anticipated as new, high-quality space continues to be absorbed.

Macroeconomic Backdrop

Portugal’s economy is expected to grow between 1.8% and 2.3% in 2026, outperforming the wider Euro Area, supported by resilient private consumption, continued deployment of European Union recovery funds, and a labour market that remains comparatively tight, with unemployment forecast to ease further through 2027.

Inflation is expected to rise moderately in 2026, largely due to energy price volatility linked to geopolitical tensions in the Middle East, before resuming a downward path toward the 2% target by 2027–2028. Interest rates and bond yields have also started to diverge, with short-term rates easing while long-term yields tick upward, a dynamic that is gradually widening the spread between real estate returns and the risk-free rate.

What to Watch for the Rest of 2026

Looking ahead, most forecasts point to continued, if measured, growth in Portugal’s real estate investment market, with full-year volume projections in the range of €2.8–3.0 billion for the broader commercial market. Prime yields are generally expected to stabilise, with some further compression possible in retail given the sector’s current momentum.

Key risks to monitor include:

- Geopolitical escalation in the Middle East and its knock-on effects on energy costs and the disbursement of EU recovery funds

- Inflationary resurgence, which could prompt central banks to pause or reverse their easing cycles

- Continued reliance on cross-border capital, which remains more sensitive to shifts in global investor sentiment than domestic demand

Overall, Portugal’s commercial real estate market enters the rest of 2026 from a position of relative strength, anchored by tourism-driven retail and hospitality demand, constrained but resilient office and logistics fundamentals, and a residential market still searching for balance between supply and demand.